Login

Login

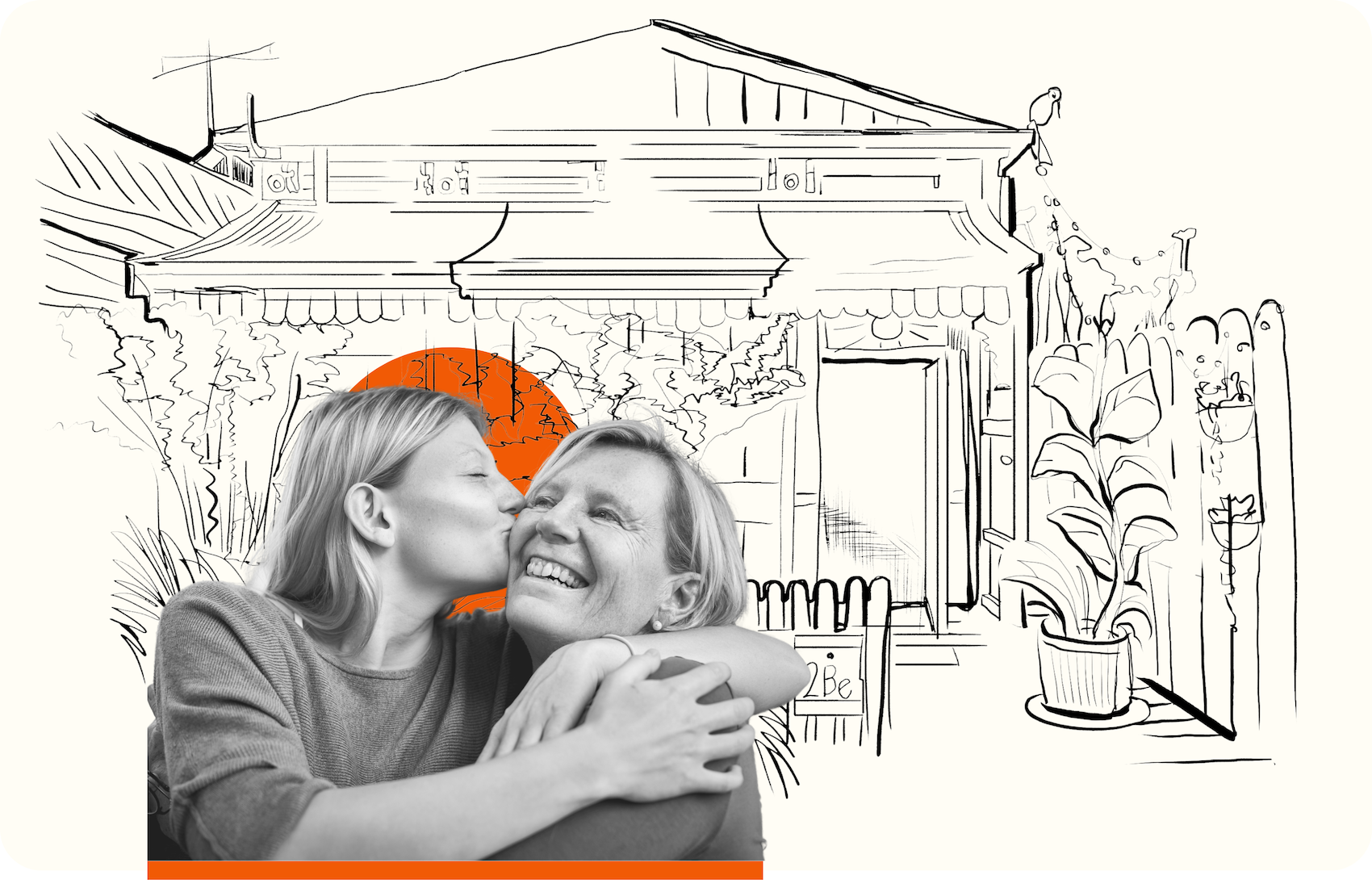

Survey finds a disconnect between the willingness of baby boomers and the reluctance of millennials to get help from the ‘’Bank of Mum and Dad’’ arrangement to get onto the property ladder.

Survey finds a disconnect between the willingness of baby boomers and the reluctance of millennials to get help from the ‘’Bank of Mum and Dad’’ arrangement to get onto the property ladder.

Two-thirds of parents say they’d like to help their children with a deposit for their first home, a new survey conducted for home equity lender 2Be has found.

But only one-third of 18 to 34-year-olds surveyed have asked or would ask their parents for help.

The results of the survey of more than 1000 Australians shows the disconnect between the willingness of baby boomers and the reluctance of millennials to get help from the ‘’Bank of Mum and Dad’’ to get onto the property ladder.

The survey, conducted for 2Be by the Evolved Group, found 60 per cent of 18 to 34-year-olds would like to buy a home in the next few years but don’t see how they can save the deposit required. However, more than half of the 530 respondents in this age group either haven’t asked or say they wouldn’t ask their parents for help.

|

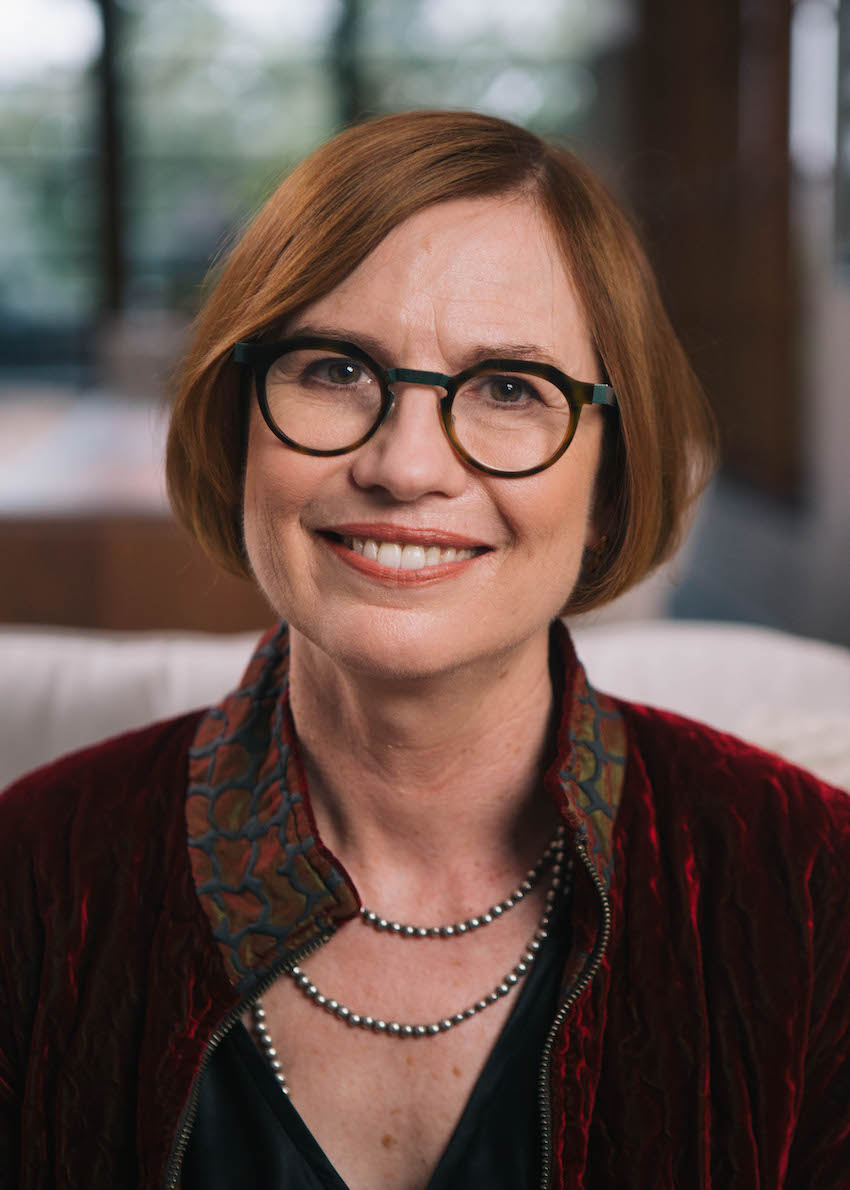

CEO of 2Be Dr Jenny Fagg said opening the ‘’Bank of Mum and Dad’’ can be fraught, particularly if there’s a difference in expectations between parents and their adult children. “We know many loans from parents to their children are undocumented, which leaves all parties vulnerable in the event of a major life event, particularly a relationship breakdown,’’ Dr Fagg said. 2Be offers free resources for families considering using parents’ home equity to help fund a child’s home deposit, including templates and checklists on its website. These educational tools help customers navigate the sometimes-difficult conversations necessary to help preserve family relationships and assets. |

There are a range of innovative products coming onto the market to help parents release the equity in their homes. Unlike the reverse mortgages of old, which gained a negative reputation after some uninformed homeowners found themselves in over their heads, the new options have a guarantee that protects borrowers from owing more than their home is worth.

2Be Equity Advantage is a home equity loan that lets homeowners between the ages of 55 and 75 access up to $500,000 of home equity by assessing a customer’s assets and credit history, rather than their income or job status. The lender’s website also provides a free equity release calculator to help parents determine how much they can borrow against their home equity.

While Equity Advantage shares some similarities with standard reverse mortgages, there are important differences as well. “At 2Be we offer a five-year fixed rate loan with a fixed interest rate, which provides customers with certainty as to the amount they will owe at the end of the term,” Dr Fagg said.

The survey also confirmed the majority of people over 55 believe that obtaining a loan from a major bank is impossible.

2Be Chairman Brian Hartzer said that since the banking royal commission, major banks have largely walked away from giving loans to people over 55, due to their focus on income serviceability.

“We know that the major lenders generally don’t lend to people in this stage of life, despite the value of their home, if they’re semi-retired or working part-time and their income doesn’t meet strict lending requirements,” Mr Hartzer said.

“However, many Australians over 55 have worked hard to own their own homes and we believe they deserve to access that equity, whether to help kids with their deposit, to fund major renovations, or to support their family’s other aspirations.”

To find out how your clients can access the equity in their home see www.2be.com.au/2be-equityadvantage

Get breaking news

You are not authorised to post comments.

Comments will undergo moderation before they get published.