Login

Login

A common trap for growing businesses and those with employees interstate due to COVID, is knowing when their total wages reach the level that requires them to register for payroll tax in the states or territories in which they have employees.

A common trap for growing businesses and those with employees interstate due to COVID, is knowing when their total wages reach the level that requires them to register for payroll tax in the states or territories in which they have employees.

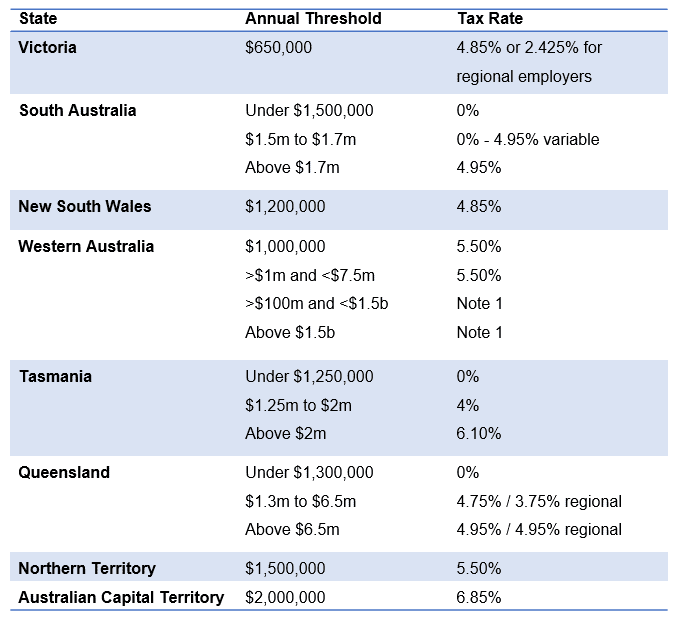

The various state revenue offices, just like the ATO, increasingly use data matching from a variety of sources (including sharing information between themselves) to test compliance with the rules, and we are seeing an increase in payroll tax investigations. Just to prove that life wasn’t meant to be simple, every state and territory has a different threshold and charges payroll tax at different rates.

Below is a summary for the year ending 30 June 2022. For payroll tax purposes, “wages” generally include any amounts of wages, salary, remuneration, commission, bonuses or allowances paid to employees, as well as taxable fringe benefits, employer superannuation contributions, benefits provided under an employee share scheme and payments to certain individuals and entities that might otherwise be regarded as contractors.

Tax-free threshold

The second common risk for a growing business is when they are registered for payroll tax in their home state but have one or two interstate employees.

The risk of this occurring has been exacerbated in the last two years with the COVID-driven explosion in remote working, with the realisation that many employees can work from anywhere, and that the technology we now use everyday makes it much easier to work across state and international borders.

Someone can be working just down the corridor, several suburbs away or on the other side of the country and it might make little difference to the way that they do their job, but it can have a notable impact on their employer’s payroll tax obligations.

Businesses with employees physically working in another state or territory must report their taxable Australian wages in each state, applying the relevant tax-free threshold and then apportioning the excess over the threshold to each state (the method used to do this calculation varies for each state and territory). The effect will be firstly that they will need to register and start paying tax on wages relating to the second state, and secondly this will increase the payroll tax payable in the home state.

Take the example of Alpha Pty Limited, which has 15 employees in NSW and total annual wages of $1.5 million, and therefore has a NSW payroll tax liability for 2022 of $14,550. Say that on 1 July 2021 Alpha takes on three employees working in Queensland for total additional salary costs of $500,000. It does not matter for these purposes whether or not the business has interstate operations or customers.

Total Australian wages will now be $2.0 million, of which 75 per cent relates to NSW wages and 25 per cent to Queensland wages. For NSW the payroll tax will now be $29,100 (i.e. [$2,000,000 – $1,200,000] x 4.85 per cent x 75 per cent), while in Queensland the payroll tax will be $10,390 (calculated on the Queensland OSR website), so Alpha will pay total payroll tax of $39,490.

Grouping of related entities

A very common payroll tax trap is the extremely wide grouping rules, which can apply to entities within the same state, and also to related entities in different states.

When entities are grouped in the same state, only one member (referred to as the designated group employer) will usually claim the tax-free threshold while all other members will be taxed at the applicable flat rate on all of their wages for the period. However, when entities are grouped in different states, the thresholds are apportioned according to the total annual Australian taxable wages.

There are several different grouping rules that can apply including where one entity controls another, or where they are both controlled by a third entity. Controlling interests can be established by direct holdings or may be indirect by tracing through interposed entities (which is where some unexpected outcomes may arise, especially where trusts are used in the structure).

Let’s vary Example 1 and have Alpha establish a subsidiary company Beta Pty Limited that runs Queensland operations, which is to be owned 60 per cent by Alpha and 20 per cent each by the two Queensland sales representatives. Clearly Alpha has a controlling interest in Beta, so they will be considered grouped for both NSW and Queensland payroll tax purposes.

As in Example 1, there will be an apportionment of the NSW payroll tax threshold and Queensland payroll tax threshold with the calculation resulting in the same outcome, a total payroll tax of $39,490, i.e. Alpha will pay $29,100 in NSW, and Beta will pay $10,390 in Queensland.

Note 1: 5 per cent for wages up to $100 million + 6 per cent for wages from $100 million to $1.5 billion + 6.5 per cent for wages above $1.5 billion

Peter Bembrick is a partner at HLB Mann Judd Sydney.

Get breaking news